The present analysis, using the NLSY97, attempts to model the structural relationship between the latent second-order g factor extracted from the 12 ASVAB subtests, the parental SES latent factor from 3 indicators of parental SES, and the GPA latent factor from 5 domains of grade point averages. A structural equation modeling (SEM) bootstrapping approach combined with a Predictive Mean Matching (PMM) multiple imputation has been employed. The structural path from parental SES to GPA, independently of g, appears to be trivial in the black, hispanic, and white population. The analysis is repeated for the 3 ACT subtests, yielding an ACT-g latent factor. The same conclusion is observed. Most of the effect of SES on GPA appears to be mediated by g. Adding grade variable substantially increases the contribution of parental SES on the achievement factor, which was partially mediated by g. Missing data is handled with PMM multiple imputation. Univariate and multivariate normality tests are carried out in SPSS and AMOS, and through bootstrapping. Full result provided in EXCEL at the end of the article.

1. Introduction.

According to Jensen (1998, chap. 14) the IQ g factor “is causally related to many real-life conditions, both personal and social. All these relationships form a complex correlational network, or nexus, in which g is the major node” (p. 544). There could be some mediation through g between past economic status (e.g., familial SES) and future status. In a longitudinal study, for example, g would be the most (or one of) meaningful predictor of future outcome such as social mobility (Schmidt & Hunter, 2004), even controlling for SES, as evidenced from sibling studies of the sibling differences in IQ/g (Murray, 1998). On the other hand, non-g component of IQ tests do not have meaningful predictive validity (Jensen, 1998, pp. 284-285) in terms of difference in incremental R² (when non-g is added after g versus when g is added after non-g).

The fact that complexity (of occupation) will mediate the relationship between IQ and income (Ganzach et al., 2013) or job complexity mediating IQ-performance correlation (Gottfredson, 1997, p. 82) is in line with suggestion that cognitive complexity is the main ingredient in many g-correlates (Gottfredson, 1997, 2002, 2004; & Deary, 2004). The decline in standard deviation (SD) in IQ scores with increasing occupational level also supports this interpretation (Schmidt & Hunter, 2004, p. 163) as it would mean that success depends on a minimum cognitive threshold that tends to increase at higher levels of occupation.

Opponents of such interpretation usually argue that IQ tests measure nothing more than knowledge, mostly based on school and experiences, and that the question of complexity is irrelevant. This assumption can’t readily explain individual and group differences on tests that are proven to be impervious to learning and practice and, instead of being dependent on knowledge, merely reflect the capacity for mental transformation or manipulation of the item’s elements in tests that are relatively culture-free (e.g., Jensen, 1980, pp. 662-677, 686-706; 2006, pp. 167-168, 182-183). Because the more complex jobs depend less on job knowledge, they have less automatable demands which is analogous to fluid g rather than crystallized g (Gottfredson, 1997, pp. 84, 97; 2002, p. 341). Additionally, the declining correlation between experience and job performance over the years (Schmidt & Hunter, 2004, p. 168) suggests that lengthy experience (e.g., through accumulated knowledge) does not compensate for low IQ. Knowledge simply doesn’t appear as the active ingredient underlying the IQ-success association.

There have been suggestions that covariations between g and social status works through an active gene-environment correlation as individuals increasingly shape their life niches over time (Gottfredson, 2010). To illustrate this, Jensen (1980, p. 322) explains that success itself (e.g., due in part to higher g) acts as a motivational factor magnifying the advantage of having a higher IQ (g) level. Or the reverse when failures accumulate over time.

Gottfredson (1997, p. 121) and Herrnstein & Murray (1994, ch. 21-22) expected that, over time, the cognitive load of everyday life would tend to increase; Gottfredson believed that to be the inevitable outcome of societies’ modernization, and Herrnstein & Murray propose a complement, which is government’s laws make life more cognitively dependent because of the necessity to deal, cope with the new established laws. Theoretically, this sounds fairly reasonable. Given this, we should have expected IQ-correlates (notably with the main variables of economic success) to have increased over the past few decades. Strenze (2007) said there wasn’t any trend at all. Several explanations include range restriction in years (1960s-1990s in Strenze data) which is obvious because there wasn’t probably any drastic change in life within this “short” period of time. Another explanation could be that, over time, all other things are not equal, i.e., other alternative factors fluctuate in both directions and could have masked the relationship between cognitive load and time.

2. Method.

I will demonstrate presently that parents’ SES predicts children’s achievement (GPA+educational years) independently of g but also through g (ASVAB or ACT) by use of latent variable approach. Next, I use a latent GPA as independent var.

2.1 Data.

Of use presently is the NLSY97. Available here (need free account). The variables included in the CFA-SEM model are parental income (SQRT applied in order to respect distribution normality), mother and father education, and GPA english, foreign languages, math, social science, life science, and the 12 ASVAB subtests. All these variables have been age/gender adjusted, except parental grade/income. Refer to the syntax here.

To be clear with the ASVAB subtests :

GS. General Science. (Science/Technical) Knowledge of physical and biological sciences.

AR. Arithmetic Reasoning. (Math) Ability to solve arithmetic word problems.

WK. Word Knowledge. (Verbal) Ability to select the correct meaning of words presented in context and to identify best synonym for a given word.

PC. Paragraph Comprehension. (Verbal) Ability to obtain information from written passages.

NO. Numerical Operations. (Speed) Ability to perform arithmetic computations.

CS. Coding Speed. (Speed) Ability to use a key in assigning code numbers to words.

AI. Auto Information. (Science/Technical) Knowledge of automobile technology.

SI. Shop Information. (Science/Technical) Knowledge of tools and shop terminology and practices.

MK. Math Knowledge. (Math) Knowledge of high school mathematics principles.

MC. Mechanical Comprehension. (Science/Technical) Knowledge of mechanical and physical principles.

EI. Electronics Information. (Science/Technical) Knowledge of electricity and electronics.

AO. Assembling Objects. (Spatial) Ability to determine how an object will look when its parts are put together.

More information on ASVAB (here) and transcript (here).

2.2. Statistical analysis.

SPSS is used for EFA. AMOS software is used for CFA and SEM analyses. All those analyses have assumptions. They work best with normally distributed data (univariate and multivariate) and continuous variables. AMOS can still perform SEM with categorical variables using Bayesian approach. Read Byrne (2010, pp. 151-160) for an application of Bayesian Estimation.

Structural equation model is a kind of multiple regression which allows us to decompose the correlations into direct and indirect paths among construct (i.e., latent) variables. We can see it as a combination of CFA and path analysis. There is a huge difference between path analysis and SEM in the sense that a latent variable approach (e.g., SEM) has the advantage of removing measurement errors in estimating the regression paths. This results in higher correlations. There is no certainty for minimum N. The golden rule is N>200, but some examples include N of 100 or 150 that work well (convergence and proper solution).

CFA requires continuous and normally distributed data (When the data variables are of ordinal type (e.g., ‘completely agree’, ‘mostly agree’, ‘mostly disagree’, ‘completely disagree’), we must rely on polychoric correlations when two variables are categorical or polyserial correlations when one variable is categorical and the other is continuous. CFA normally assumes no cross-loadings, that is, subtests composing the latent factor “Verbal” are not allowed to have significant loadings on another latent factor, e.g., Math. Even so, forcing a (CFA) measurement model to have zero cross-loadings when EFA reveals just the opposite will lead to misspecification and distortion of factor correlations as well as factor loadings (Asparouhov & Muthén, 2008).

But when there are cross-loadings, it is said that there is a lack of unidimensionality or lack of construct validity, in which case, for instance, parceling (i.e., averaging) items is not recommended as indicators to be used in building a latent factor (Little et al., 2002). Having two (or more) latent factors is theoretically pointless if the observed variables load on every factors, in which case we should not have assumed the existence of different factors in the first place.

It is possible to build latent factors in SEM with only one observed variable. This is done by fixing the error term of that observed variable to a constant (e.g., 0.00, 0.10, 0.20, …). But even fixing the (un)reliability of that ‘latent factor’ does not means it should be treated or interpreted as a truly latent factor because in this case it is a “construct” by name only.

By definition, a latent variable must be an unobserved variable assumed to cause the observed (indicator) variables. In this sense, he is called a reflective construct, and this is why the indicators have arrows going into them with an error term. The opposite is a formative construct where the indicators are assumed to cause the construct (which becomes a weighted sum of these variables), and this is why the construct itself has an arrow going into him with an residual (error term, or residual variance). This residual represents the “represents the impact of all remaining causes other than those represented by the indicators included in the model” (Diamantopoulos et al., 2007, p. 16). Hence the absence of residual term is an indication that formative indicators are modeled as to account for 100% of the variance in the formative construct, a very unlikely assumption.

If we want to perform a formative model, a special procedure is needed to achieve identification (MacKenzie et al., 2005, p. 726; Diamantopoulos et al., 2007, pp. 20-24). For example, instead of having three verbal indicators caused by a latent verbal, we must draw the arrows from those (formative) indicators to the latent and then fix one of these paths to 1, and each formative construct having at least 2 (unrelated) observed variables and/or reflective latent variables that are caused by this formative construct. Finally, the formative indicators causing the construct should covary (double headed arrow) among them. Given the controversy and ongoing debate surrounding the formative models and by extension the MIMIC (multiple indicator multiple cause) models, I will just ignore this approach. The kind of latent variables used presently are of reflective kind.

2.2.1. Fundamentals.

a) Practice.

AMOS output usually lists 3 models : 1) default 2) saturated 3) independence model. The first illustrates the model we have specified (actually could be called reduced model, or over-identified), this is the one we are interested in. The second is a (full) model that assumes everything is related to everything (just-identified) with direct path from each variable to each other; it has a perfect fit but this in itself is meaningless. The third assumes that nothing is related to anything, or the null model (no parameters estimated).

In SEM, the model needs to be well specified. Otherwise the model is said to be misspecified (disparity between real-world relationships and model relationships), either because of over-specification (contrain irrelevant explanatory variables) or under-specification (absence of relevant explanatory variables). This can occur when the model specifies no relationship (equal to zero) between two variables when their correlation was in fact non-zero.

Some problems in modeling can even cause the statistical program to not calculate parameters estimates. There can be “under-identification” which causes troubles with the model. This appears when there are more unknown parameters than known parameters, resulting in negative degrees of freedom (df). At the Amos 20 User’s Guide, page 103 displays a structural path diagram with the explanation about how to make the model identified.

To better understand the problem of (non)identification, just use an example with 3 variables, X, Y, Z. This means we have 6 pieces of information : the variance for each variables X, Y, and Z, thus 3 variances, plus the covariance of each variables with one another, that is, X with Y, Y with Z, X with Z, thus 3 covariances. Identification problems emerge when the number of freely estimated parameters exceeds the pieces of information available in the actual sample variance-covariance matrix.

Concretely, such model 3 (knowns) – 4 (unknowns; to be estimated) = -1 df is clearly no good because calculation of the model parameters cannot proceed. Thus, more constraints need to be imposed in order to achieve identification. If, on the other hand, the df is equal to zero, the model is said to be “just-identified”, meaning there is a unique solution for the parameters while goodness of fit cannot be computed. In that case, the model fit with regard to the data is perfect. And if df is greater than zero (more knowns than unknows) the model is said to be “over-identified”, which means that there are multiple solutions for at least some of the parameters. The best solution is chosen through maximization of the maximum likelihood function. However, there is no need to worry so much about model identification. AMOS won’t run or calculate the estimates if df is negative. This is seen in the panel left to the “Graphics” space, where the default model would have an “XX” instead of an “OK”.

Remembering what df is, is relevant to the concept of model parsimony and complexity. The more degrees of freedom the model has, and the more parsimonious it is. The opposite is model complexity which can be thought as the greater number of free parameters (i.e., unknowns to be estimated) in a model. Lower df indicates more complex models. Complexity can be increased just by adding more (free) parameters, e.g., paths, covariances, and even cross-loadings. To be sure, freeing a parameter means we allow the unknown (free) parameter to be estimated from the data. Free parameters are the added paths, covariance, or variables (exogenous or endogenous) that do not have their mean and variance fixed at a given value. But doing so has serious consequences on model fit when fit indices penalize for higher model complexity (see below).

In SEM, it is necessary to achieve identification by, among possibilities, fixing one of the factor loadings of the indicator (observed) variables at 1. The (observed, not latent) variable receiving this fixed loading of 1 is usually called a marker variable. It allows the variables to be expressed in the same scale, and thus are seen as standardized variables (with mean of 0, variance of 1). It does not matter which variable is chosen as marker, it does not affect estimates or model fit. Alternatively, we can select the latent factor and fix its variance at 1, the problem however emerges when this latent variable has an arrow going into him because in that case AMOS will not allow the path to be defined unless we suppress the constrained variance of 1 as AMOS requires.

Among other identification problems are the so-called empirical under-dentification, occuring when data-related problems make the model under-identified even if the model is theoretically identified (Bentler & Chou, 1987, pp. 101-102). For example, latent factors need normally 3 indicators at minimum, and yet the model will not be identified if one factor loading approaches zero. And similarly for a two-factor model that needs the correlation/covariance between the factors to be nonzero.

In SEM, parameters are the regression coefficients for paths between variables but also variance/covariance of independent variables. In the structural diagrams, the dependent or criterion variable(s) is (are) those having (receiving) a single-headed arrow going into them and not starting from them. They are called endogenous variables, as opposed to exogenous (i.e., predictor) variables. The covariances (non-causal relationship) are illustrated as curved double-headed arrows and, importantly, they cannot be modeled among endogenous variables or between endogenous and exogenous variables. Covariances involve only exogenous variables. And these exogenous var. should not have error terms because they are assumed to be measured without error (even though this assumption may seem unrealistic). AMOS would assume no covariance between exogenous var., if there is no curved double-headed arrow linking them or if that arrow has a covariance value of zero (see AMOS user guide, p. 61). Either way, this is interpreted as a constraint (not estimated by the program). Likewise, AMOS assumes a null effect of one variable on another if no single-headed arrow linked these two.

Here, the large circles are latent variables, small circles are called errors (e1, e2, …) or residuals in the case of observed (manifest) variables and disturbances (D) in the case of latent variables, and rectangles the observed variables (what we have in our raw data set).

In the above picture, we see the following number related to the disturbance of the latent SES : ‘0.’ … where the number on the left of the comma designates the mean of the error term, which is fixed at zero by default. The number on the right of the comma designates the variance of the error term. The absence of any number indicates we want to freely estimate the error variance; otherwise we can fix it at 0 or 1, or any other number between 0 and 1. But if we want to constrain the error/variable variances to be equal, we can do so by assigning them a single label (instead of a number) identical for all of them (AMOS user guide, pp. 43-45).

Again, if we decide not to fix the mean, there should be no number associated to the error term or latent factor. To do this, click on the circle of interest, and specify the number (0 or 1) we want to be fixed, or the number to be removed if we decide not to fix it at a constant.

Above we see the two predictor variables (ASVAB and SES) sharing a curved double-headed arrow, that is, they covary. In this way, we get the independent impact of X1 on Y controlled for the influence of X2, and the impact of X2 on Y controlled for X1. When reporting the significance of the mediation, it is still possible to report the standardized coefficient with the p-value of the unstandardized coefficient.

b) Methodological problems.

In assessing good fit in SEM, we must always proceed in two steps. First, look at the model fit for measurement model (e.g., ASVAB models of g) and, second, look at the structural model connecting the latent variables. In doing so, when a bad fit is detected, we can locate where it originates : the measurement or the structural portion of the SEM model.

When it comes to model comparisons (target versus alternative), Tomarken & Waller (2003, p. 583) noticed that most researchers do not acknowledge explicitly the plausibility of the alternative model(s) they were testing. If we had two predictors (X) affecting one outcome (Y) variables, and that in the real world, the two predictors are very likely to be related (say, scholastic tests and years of schooling), a model that assumes the two predictors to be uncorrelated is not plausible in real life, and therefore the alternative model has no meaning. The best approach would be to compare two (theoretically) plausible models because a model by definition is supposed to represent a theory having real-life implications.

In SEM, the amount of mediation can be defined as the reduction of the effect of X on Y variable when M is added as mediation. Say, X->Y is labeled path C in the model without M, and X->Y is labeled path C’ in the model with M whereas X->M is labeled A and M->Y is labeled B. And by this, the amount of mediation is the difference between C and C’ (C-C’) and the mediation path AB is equal to C-C’. The same applies for moderator variables; say, variables A, B, AxB (the interaction) and Y in model 1, with variables A, B, AxB, M (the mediation) and Y in model 2, where the difference in the direct path AxB->Y between model 1 and 2 is indicative of the attenuation due to the mediator M. See Baron & Kenny (1986) for a discussion of more complex models.

The pattern of a mediation can be affected by what Hopwood (2007, p. 266) calls proximal mediation. If the variable X causes Y through mediation of M variable, X will be more strongly related to M than Y to M if the time elapsed between X and M is shorter (say, 2 days) than between Y and M (say, 2 months). Conversely, when we refer to distal mediation if M is closer (in time) to Y, resulting in overestimation of M->Y and underestimation of X->M.

Hopwood (2007, p. 264) also explains how moderators (interaction effects) and curvilinear functions (effect varying at certain levels of M) can be included in a model. For X and M causing Y, we add an additional variable labeled XM (obtained by simply multiplying X by M, could be done in SPSS, for instance) causing Y. Furthermore, we add two additional variables, squared M and squared XM. The regression model is simply illustrated as follows : X+M+XM+M²+XM²=Y. Here, the XM² represents the curvilinear moderation. Gaskin has a series of videos describing the procedure in AMOS (Part_7, Part_8, Part_9, Part_10). See also Kline (2011, pp. 333-335). Although one traditional way of testing moderation is by comparing the effect of X on Y separately in the different groups (gender, race, …), if there was a difference in the relationship across the groups, an interaction effect may be thought to be operating. Nonetheless, this method is problematic because variance in X may be unequal across levels of M. In this case, differing effects of X on Y across levels of M are attributed to difference in range restriction among the groups, not moderation effect. Also, if measurement error of X is seen to differ across levels of M, this would be evidence of moderation effect (X->Y varying across levels of M). Latent variable approach (e.g., SEM) hopefully tends to attenuate this concerns. Note that an unstandardized regression coefficient, unlike correlation, is not affected by the variance of independent var. or measurement error in dependent var., and Baron & Kenny (1986, p. 1175) recommend their use in this case.

The construction of moderator variables in SEM has the advantage that it attenuates the measurement errors usually associated with the interaction term (Tomarken & Waller, 2005, pp. 45-46) although their use can have some complications (e.g., specifications and convergence problems). The typical way is to multiply all of the indicators (a1, a2, …) of the latent X by the indicators (b1, b2, …) of the latent M, such as a1*b1, a1*b2, a2*b1, a2*b2 and then by creating the latent variable using all of these interaction variables (see here). The same procedure is needed when modeling quadratic effect, e.g., creating a latent variable X² with a1^2, a2^2, and so on. Alternatively, Hopwood (2007, p. 268) proposes to conduct factor analysis with Varimax, to save the standardized factor score, and to create the interaction variable by multiplying these factor score variables.

In some scenarios, measurement errors can be problematic (Cole & Maxwell, 2003, pp. 567-568). When X is measured with error but not M and Y, the path X->M will be downwardly biased while M->Y and X->Y will be unaffected. For example, with X’s reliability of 0.8, a path of 0.8 assuming perfect reliability will then become 0.8*(SQRT(0.8))=0.72. When Y only is measured with error, only the path M->Y is biased. But when M is measured with error, the (direct) path X->Y is upwardly biased while the other two (indirect) paths are underestimated. Again, the latent variable approach is an appropriate solution for dealing with this problem. And this is one of the great advantage of SEM over simple path analysis.

In a longitudinal design, method shared variance can upwardly bias the correlations between factors when factors are measured by indicators assessed by the same method (or measure) rather than by different methods (e.g., child self-report vs. parent self-report). In the field of intelligence, method must be equivalent to the IQ tests measuring a particular construct (verbal, spatial, …) when the same measure is administered several times at different points in time. But repeated measures (or tests) over time is virtually impossible to avoid in longitudinal data (e.g., CNLSY79), so that such effect must be controlled by allowing correlated errors of same-method indicators across factors. In all likelihood, the correlation (or path) between factors would be diminished because the (upward biased) influence of method artifacts on the correlation have been removed. See Cole & Maxwell (2003, pp. 568-569). Several data analysts (Little et al., 2007; Kenny, 2013) added that we should test for measurement invariance of factor loadings, intercepts, and error variances, if we want to claim that the latent variable remains the “same” variable at each assessment time. Weak invariance (factors) is sufficient for examining covariance relations but strong invariance (intercepts) is needed to examine mean structures.

The same authors also address the crucial question of longitudinal mediation. Most of the studies use cross-sectional mediation, all the data having been gathered at the same time point. There is no time elapsing between the predictor, mediator and outcome (dependent) variables. Causal inferences are not possible. The choice of variables is important too. Retrospective measures are not recommended, for example. Other measures such as background can hardly be viewed as causal effects because these variables (e.g., education level) don’t move over time. But some others (e.g., income and job level) can move up and down over years.

In some cases, researchers proceed with an half-longitudinal approach, e.g., predictor (X) and mediator (M) measured at time #1, and outcome (Y) at time #2. They argue such approach is not appropriate either, that X->M will be biased because X and M coincide in time and that prior level of M is not controlled. Likewise, when M and Y have been assessed at the same time, but not X, then M->Y will be biased. Ideally, causal models must control for previous levels of M when predicting M and control for previous levels of Y when predicting Y. Using half-longitudinal design with 2 waves, we can still use X1 to predict M2 controlling for M1 and use M1 to predict Y2 controlling for Y1. See Little et al. (2007, Figure 3) for a graphical illustration. Although such practice is less bias-prone, we can only test whether M is partial mediator but not if M could be a full mediator. Furthermore, we cannot test for violation of the stationarity assumption. Stationarity denotes an unchanging causal structure, that is, the degree to which one set of variables produces change in another set remains the same over time. For example, if longitudinal measurement invariance (e.g., by constraining a given parameter to equal its counterparts at the subsequent waves) is violated, the stationarity assumption would be rejected.

Of course, the point raised by Cole & Maxwell (2003) is not incorrect but what they want is no less : predictor(s) at time1, mediator(s) at time2, outcome at time3. In other words, 3 assessment occasions. Needless to say, this goal is, in practice, virtually impossible to achieve by an independent, small team, with limited resources.

2.2.2. CFA-SEM model fit indices.

A key concept of SEM is to evaluate the plausibility of hypotheses modeled through SEM. Concretely, it allows model comparison by way of model fit indices. The best fitted model is selected based on these fit indices. A good fit is indicative that the model reproduces the observed covariance accurately but not necessarily that exogenous and mediators explain a great portion of the variance in the endogenous variables; even an incorrect model can be made to explain the data just by adding parameters to the point where df falls to zero. Associations and effects can be small with good model fit, if residual variances (% unexplained; specificity+error) are sufficiently high as to generate equality in the implied and observed variances (Tomarken & Waller, 2003, p. 586).

Browne et al. (2002) argue that very small residuals in observed variables, while suggesting good fit, could easily result in poor model fit as indicated by fit indices, in factor analysis and SEM. But the explanation is that fit indices are more sensitive to misfit (misspecifications) when unique variances are small than when they are large. Hence, “one should carefully inspect the correlation residuals in E (i.e., the residual matrix, E=S-Σ where s is sample data covariance and Σ fitted or implied covariance). If many or some of these are large, then the model may be inadequate, and the large residuals in E, or correspondingly in E*, can serve to account for the high values of misfit indices and help to identify sources of misfit.” (p. 418). The picture is thus complicated to the extent that all this means we should not rely exclusively on fit indices (with the exception of RMR/SRMR computed using these same residual correlation matrices) because they can be very inaccurate sometimes. Hopefully, the situation where error and specificity are so small as to reflect observed variables as being very high accurate measures of latent variables is likely to be rare.

Unfortunately, the reverse phenomenon is true. In a test of CFA models, Heene et al. (2011) discovered that decreasing factor loadings (which consequently increases unique variances) under any of these two kinds of misspecified models, 1) simple, incorrectly assuming no factor correlation, 2) complex, incorrectly assuming no factor correlation and no cross-loading, will cause increasing good model fitting, as a result of altering the statistical power to detect model misfit. In this way, a model would be validated by fit indices (e.g., χ²) erroneously. Even the popular RMSEA, SRMR and CFI are altered by this very phenomenon. Another gloomy discovery is the lack of sensitivity to misspecification (i.e., capability of rejecting models) for RMSEA when the number of indicators per factor (i.e., free parameters) increases, irrespective of factor loadings. Regarding properly specified models, it seemed that χ² and RMSEA are not affected by loadings size while SRMR and CFI could be.

Similarly, Tomarken & Waller (2003, p. 592, Fig.8) noted that, in typical SEM models, the power to detect misspecification, holding sample size constant, depend on 1) the magnitude of factor loadings and 2) the number of indicators per latent factors. Put it otherwise, the power to detect any difference in fit between models improves when 1) or 2) increases, but this improvement depends on sample size (their range of N was between 100 and 1000).

There are three classes of goodness-of-fit indices : absolute fit (χ², RMR, SRMR, RMSEA, GFI, AGFI, ECVI, NCP) which considers the model in isolation, incremental fit (CFI, NFI, (TLI) NNFI, RFI, IFI) which compares the actual model to the independent model where nothing is correlated to anything, and parsimonious fit (PGFI, PNFI, AIC, CAIC, BCC, BIC) adjusts for model parsimony (or df). An ideal fit index is one that is sensitive to misspecification but not to sample size (and other artifacts). What must be avoided is not necessarily trivial misspecification but the severe misspecification. Here’s a description of the statistics commonly used :

The χ²/df (CMIN/DF in AMOS), also called relative chi-square, is like a badness of fit, with higher values denoting bad fit because it evaluates the difference between observed and expected covariance matrices. However, χ² is too sensitive. The χ² increases with sample size (e.g., like NFI) and its value diminishes with model complexity due to reduction in degrees of freedom, even if the χ² divided by degrees of freedom overcomes some of its shortcomings. This index evaluates the discrepancy between the actual (and independence) model and the saturated model. The lower, the better. AMOS also displays p-values, but we never see a value like 0.000. Instead we have *** which means it’s highly significant. The p-value here is the probability of getting as large a discrepancy as occurred with the present sample and, so, is aimed to test the hypothesis that the model fits perfectly in the population.

In AMOS, PRATIO is the ratio of how many paths you dropped to how many you could have dropped (all of them). In other words, the df of your model divided by df of the independence model. The Parsimony Normed Fit Index (PNFI), is the product of NFI and PRATIO, and PCFI is the product of the CFI and PRATIO. The PNFI and PCFI are intended to reward those whose models are parsimonious (contain few paths) that is, adjusting for df. What is called the model parsimony is one that is less complex (less parameterized), making less restricted assumptions (think about Occam’s Razor).

The AIC/CAIC, BCC/BIC are somewhat similar to the χ² in the sense that it evalutes the difference between observed and expected covariances, low values are therefore indicative of better fit. Like the χ²/df, they adjust for model complexity. Absolute values for these indices are not relevant. What really is important is the relative index in comparing between models. Despite AIC being commonly reported, it has been criticized due to its tendency to favor more complex models as sample size (N) increases because the rate of increase in the badness of fit term increases with N even though its penalty term remains the same (Preacher et al., 2013, p. 39). AIC also requires sample size of 200 (minimum) to make its use reliable (Hooper et al., 2008). Unlike AIC, CAIC adjusts for sample size. For small or moderate samples, BIC/BCC often chooses models that are too simple, because of its heavy penalty (more than AIC) on complexity. Sometimes, it is said that BCC should be preferred over AIC.

The Adjusted (or not) Goodness of Fit Index (GFI, AGFI) should not be lower than 0.90. The higher, the better. The difference between GFI and AGFI is that AGFI adjusts for the downward biasing effect resulting from model complexity. These indices evaluate the relative amount of variances/covariances in the data that is predicted by the actual model covariance matrix. GFI is downwardly biased with larger df/N ratio, and could also be upwardly biased with larger number of parameters and sample size (Hooper et al., 2008). GFI is not sensitive to misspecification. Sharma et al. (2005) concluded that GFI should be eliminated. Note also that AGFI remains sensitive to N.

The PGFI and PNFI, respectively Parsimony Goodness-of-Fit Index and Parsimony Normed Fit Index, are used for choosing between models. We thus look especially at the relative values. Larger values indicate better fit. PGFI is based upon GFI and PNFI on NFI but they both adjust for df (Hooper et al., 2008). Both NFI and GFI are not recommended of use (Kenny, 2013). There is no particular recommended threshold (cut-off) values for them.

The comparative fit index (CFI) should not be lower than 0.90, this value is an incremental fit index which shows the improvement of a given model compared to the baseline (or null) model in which all variables are allowed to be uncorrelated. It declines slightly in more complex models and it is one of the measures least affected by sample size. By way of comparison, the TLI (sometimes called NNFI, non-normed fit index) is similar but it displays a lower index than CFI. Kenny (2013) recommends TLI over CFI, the former giving more penalty for model complexity (CFI adds a penalty of 1 for every parameter estimated). MacCallum et al. (1992, p. 496) and Sharma et al. (2005) found however that NNFI (TLI) is quite sensitive to sample size but this is a function of the number of indicators. Hooper et al. (2008) conclude the same, NNFI being higher in larger samples, just like the NFI. Also, due to its nature of being a non-normed value, it can go above 1.0 and consequently generates outliers when N is small (i.e., ~100) or when factor loadings are small (i.e., ~0.30).

RMSEA estimates the discrepancy related to the approximation, or the amount of unexplained variance (residual), or the lack of fit compared to the saturated model. Unlike many other indices, RMSEA provides its own confidence intervals (narrower lower/upper limits reflecting high precision) that measure the sampling error associated with RMSEA. The RMSEA should not be higher than 0.05, but some authors recommend the 0.06, 0.07, 0.08 and even 0.10 threshold cut-off. The lower, the better. In principle, this index directly corrects for model complexity, as a result, for two models that explain the data equally well, the simpler model has better RMSEA fit. RMSEA is affected by low df and sample size (greater values for smaller N) but not substantially, and can possibly become insensitive to sample size when N>200 (Sharma et al., 2005, pp. 938-939). These authors also indicate that the index is not greatly affected by the number of observed variables in the model, but Fan & Sivo (2007, pp. 519-520) and Heene et al. (2011, p. 327) reported that RMSEA declines considerably with higher number of observed variables (i.e., larger model size), which is the exact opposite of CFI and TLI that would indicate worse fit (although not always) as the number of indicators increases. In fact, it seems that most fit indices are affected by model types (e.g., CFA models vs. model with both exogenous and endogenous latent variables) to some extent. For this reason, Fan & Sivo (2007) argue that it is difficult to establish a flawless cut-off criteria for good model fit. Same conclusion has been reached by Savalei (2012) who discovered that RMSEA becomes less sensitive to misfit when the number of latent factors increases, holding constant the number of indicators or indicators per factor.

The RMR (Root Mean Square Residual) and SRMR (standardized RMR) again express the discrepancy between the residuals of the sample covariance matrix and the hypothesized covariance model. They should not be higher than 0.10. That index is an average residual value calculated using the residualized covariance matrix (equal to the fitted variance-covariance matrix minus sample variance-covariance matrix, and displayed in AMOS through “Residual moments” option) where the absolute standardized values >2.58 are considered to be large (Byrne, 2010, pp. 77, 86). It is interpreted as meaning that the model explains the correlations to within an average error of, say, 0.05, if the SRMR is 0.05. Because RMR and SRMR are based on squared residuals, they give no information about the direction of the discrepancy. RMR is difficult to interpret because it is dependent on the scale of observed variables, but SRMR corrects for this defect. The fit index for SRMR is lower with more parameters (or if the df decreases) and with larger sample sizes (Hooper et al., 2008). In AMOS, the SRMR is not displayed in the usual output text with the other fit indices but in the plugins “Standardized RMR”. An empty window is opened. Leave this box opened and click on “Calculate estimates”. The box will display the value of SRMR. But only when data is not missing. So we must use imputations.

The ECVI (Expected Cross Validation Index) is similar to AIC. It measures the difference between the fitted covariance matrix in the analyzed sample and the expected covariance matrix in another sample of same size (Byrne, 2010, p. 82). Smaller values denote better fit. ECVI is used for comparing models, hence the absence of threshold cut-off values for an acceptable model. Like AIC, the ECVI tends to favor complex models as N increases (Preacher, 2006, p. 235) because more information accrues with larger samples and models with higher complexity can be selected with greater confidence, whereas at small sample sizes these criteria are more conservative.

That being said, all statisticians and researchers would certainly affirm that it is necessary to report the χ² and df and associated p-values, even if we don’t trust χ². In my opinion, I would say it is better to report all indices we can. Different indices reflect different aspect of the model (Kline, 2011, p. 225). We must rely on fit indices but also on the interpretability of parameter estimates and theoretical plausibility of the model.

The rule of thumb values is arbitrary, varying with authors, and for this reason it is not necessary to follow these rules in a very strict manner. Cheung & Rensvold (2001, p. 249) rightly point out that fit indices are affected by sample size, number of factors, indicators per factor, magnitude of factor loadings, model parsimony or complexity, leading these authors to conclude that “the commonly used cutoff values do not work equally well for measurement models with different characteristics and samples with different sample sizes”. Fan & Sivo (2007) even add : “Any success in finding the cut-off criteria of fit indices, however, hinges on the validity of the assumption that the resultant cut-off criteria are generalizable to different types of models. For this assumption to be valid, a fit index should be sensitive to model misspecification, but not to types of models.” (p. 527). But if we are concerned with these threshold values, it seems that CFI is the more robust index. To the best of my knowledge, it is the less criticized one.

Finally, keep in mind that fit indices can be effected by missing data rates when a model is misspecified (Davey & Savla, 2010) although that differs with the nature of the misspecification.

The AMOS user’s guide (Appendix C, pp. 597-617) gives the formulas for the fit indices displayed in the output, with their description.

2.2.3. Dealing with missing values.

Traditional methods such as pairwise and listwise deletion are now considered as non-optimal ways to deal with missing data in some situations but in some other cases, listwise yields unbiased estimates in regression analyses when the missing values in any of the independent var. do not depend on the values of the dependent var. (Allison, 2002, pp. 10-12). “Suppose the goal is to estimate mean income for some population. In the sample, 85% of women report their income but only 60% of men (a violation of MCAR, missing completely at random), but within each gender missingness on income does not depend on income (MAR, missing at random). Assuming that men, on average, make more than women, listwise deletion would produce a downwardly biased estimate of mean income for the whole population.” (Allison, 2009, p. 75). MCAR seems to be a strong assumption and is a condition rarely met in most situations.

Generally, maximum-likelihood (ML) and multiple imputation (MI) are among the most popular and recommended methods. In the MI process, multiple versions of a given dataset are produced, each containing its own set of imputed values. When performing statistical analyses, in SPSS at least, the estimates for all of these imputed datasets are pooled (but some are not, e.g., standard deviations). This produces more accurate estimates than it would be with only one (single) imputation. The advantage of MI over ML is its general use, rendering it useable for all kind of models and data. The little disadvantage of MI over ML is that MI produces different results each time we use it. Another difference is that standard errors must be (slightly) larger in MI than in ML because MI involves a random component between each imputed data sets. The MAR assumption, according to Heymans et al. (2007, p. 8) and many other data analysts, cannot be tested, but these authors cited several studies revealing that models incompatible with MAR are not seriously affected (e.g., estimates and standard errors) when multiple imputation (MI) is applied. MI appears to minimize biases. In general, MI is more robust to assumptions’ violation than ML.

A distinction worth bearing in mind is the univariate imputation (single imputation variable) and the multivariate imputation (multiple imputation variables). The univariate version fills missing values for each variable independently. The multivariate version fills missing values while preserving the relationship between variables, and we are mostly concerned with this method because in most cases, data has missing values on multiple variables. We are told that “Univariate imputation is used to impute a single variable. It can be used repeatedly to impute multiple variables only when the variables are independent and will be used in separate analyses. … The situations in which only one variable needs to be imputed or in which multiple incomplete variables can be imputed independently are rare in real-data applications.” See here.

A point worth recalling is that the use of the imputed values in the dependent variable has been generally not recommended for multiple regressions. This does not mean that the dependent var. should not be included in the imputation procedure. Indeed, if dependent var. is omitted, the imputation model would assume zero correlation between the dependent and the independent variables. Dependent var. should probably be included in the final analysis as well.

On the best practices of multiple imputation, a recommendation is the inclusion of auxiliary variables, which do not appear in the model to be estimated but can serve the purpose of making MAR assumption more plausible (Hardt et al., 2012). They are used only in the imputation process, by including them along with the other incomplete variables. Because imputation is the process of guessing the missing values based on available values, it makes sense that the addition of more information would help making the “data guessing” more accurate. These variables must not be too numerous and their correlations with the other variables must be reasonably high (data analysts tend to suggest correlations around 0.40) in order to be useful for predicting missing values. The higher the correlations, the better. Some recommended that the ratio of subjects/variables (in the imputation) should never fall below 10/1. Alternatively, Hardt et al. (2012) recommend a maximum ratio of 1:3 for variables (with or without auxiliaries) against complete cases, that is, for 60 people having complete data, up to 20 variables could be used. Auxiliary is more effective when it does not have (or fewer) missing values. This is another advantage of MI over ML.

The best auxiliary variables are identical variables measured at different points in time. Probably the best way to use auxiliaries is to find variables that measure roughly the same thing as the variables involved in the final structural models.

Early MI theorists once believed that a set of 5 imputations is well enough to provide us with a stable final estimate. But after more research, others argue now that 20-100 imputations would be even better (Hardt et al., 2012). Allison (Nov 9, 2012) affirms that it depends on the % of missing values. For instance, with 10% to 30% missing, 20 imputations would be recommended, and 40 imputations for 50% missing. More precisely, the number of imputation should be more or less similar to the % of missing values; say, for 27% missing, 30 imputations would be reasonable. I don’t have the energy to run the analysis 20 or 40 times for each racial group, so I will limit my imputations to 5 data sets. Thus, in total, the SEM mediation analysis is conducted 18 times (original data + 5 imputed data, for the 3 racial groups) for the ASVAB.

A caveat is that some variables are restricted to a particular group of subjects. For example, a variable “age of pregnancy” should be available only for women and must have missing values for all men, a variable “number of cigarettes per day” available only to people having responded “yes” to the question “do you actually smoke”. The use of imputation could fill the data for men and non-smokers, which makes no sense. A solution is the so-called “conditional imputation” that allows us to impute variables which are defined within a particular subset of the data, and outside this subset, the variables are constant. See here.

And still another problem arises when we use categorical variables in the imputation model. Say, the variables can only take on 5 values, 1, 2, 3, 4, 5, like a Likert-type scale (e.g., personality questionnaire). This variable cannot “legally” have a value of, say, 1.6, or 3.3, or 4.8. It may be that linear regression method for imputation will not be efficient in that case. To this matter, Allison (2002, p. 56) recommends to round the imputed values. Say, we impute a binary variable coded 0 and 1, and the imputed values above 0.5 can be rounded to 1, below 0.5 rounded to 0. Sometimes, the values can be outside this range (below 0, above 1) but rounding is still possible. With continuous variables, there is no such problems. Even so, a categorical variable having many values, say education or grade level with 20 values, going from 1 to 20, can be (and is usually) treated as a continuous variable. On the other hand, hot deck and PMM imputations can easily deal with categorical variables. If, instead of PMM, we use the SPSS default method “Linear Regression” we will end up with illegal values everywhere. PMM gives the actual values that are in your data set. If your binary variable has only 0 and 1, PMM gives either 0 or 1.

It is also recommended to transform non-normal variables before imputation. Lee & Carlin (2009) mentioned that symmetric distribution in the data avoids potential biases in the imputation process.

An important question that has not been generally treated is the possible between-group difference regarding the correlations of the variables of interest. Some variables can be strongly related in a given racial/sex/cohort group but less so in another group. Because the aim of the present article is to compare the SEM mediation across racial group, and given the possibility of racial differences in the correlations, it is probably safer to impute the data for each racial group separately. This is easily done through FILTER function where we specify the value of the race variable to be entered. This method can ensure us that the correlations won’t be distorted by any race or group-interaction effects, even if the obvious drawbacks emerge when we work with small data. Another possibility is to create an interaction variable between the two variables in question and to include it in the imputation model (Graham, 2009, p. 562). But this would be of no interest if the interaction between the 2 relevant variables is not meaningful.

When we compute estimates from the different imputed data, we can (should) average them. However, we should not average t-, z-, F-statistics, or the Chi-Square (Allison, 2009, p. 84). For averaging standard errors, say, we have to apply Rubin (1987) formula because a simple “averaging method” fails to take into account the variability in imputed estimations, and those statistics (standard errors, p-values, confidence intervals, …) tend to be somewhat downwardly biased. For this analysis, I have applied Rubin’s formula for pooling SE, CI and the C.R. See attachment at the end of the post.

a) Multiple imputation on SPSS.

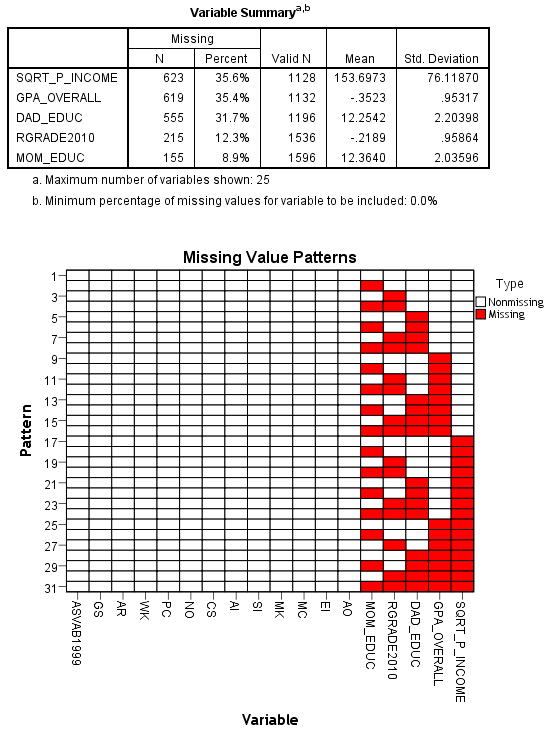

We go to “Multiple Imputation” option and then go to “Analyze Patterns” and include the variables we wish to use in SEM analysis. We get a chart that reveals the patterns of missing values in the selected variables. My window looks like this.

Initially, the minimum % of missing values is 10, but I choose to lower this value at 0.01. All of the variables supposed to be included in the CFA-SEM models should be selected. Grouping variables like “race” and “gender” are not needed here.

The chart we are interested in is the “Missing Value Patterns”. As we can see, there are clumps or islands of missing and non-missing values (cells) which means that data missingness displays monotonicity (see IBM SPSS Missing Values 20, pp. 48-49). Individuals having missing values on a given variable will also have missing values on other, subsequent variables. Similarly, monotonicity is apparent when a variable is observed for an individual, the other, previous variables are also observed for that individual. Say, we have 6 variables, var1 has no missing, 10% people are missing on var2 but also on all other variables, 10% additional are missing on var3 but also on the next variables, 10% additional are missing on var4 but also on var5 and var6, and so on. The opposite is an arbitrary missing pattern which involves impossibility of reordering the variables to form a monotonic pattern. To be sure, here’s an overview of missing data patterns, from Huisman (2008) :

Compare with what I get, below. At the bottom of this picture, there seems to be a tendency for monotonicity. But from a global perspective, the justification for a monotone imputation method is not clear to me.

SPSS offers the Fully Conditional Specification (FCS) method, also known as chained equations (MICE) or sequential regression (SRMI), which fits an univariate (single dependent variable) model using all other available variables in the model as predictors and then imputes missing values for the variable being fit. FCS is known as being very flexible, does not rely on the assumption of multivariate normality. FCS uses a specific univariate model per variable, and is a sort of variable-by-variable imputation, i.e., specifying linear regression for continuous var., logistic regression for binary var., ordinal logistic regression for categorical var. In SPSS, the FCS employs Markov Chain Monte Carlo (MCMC) method; further reading, see Huisman (2011). More precisely, it employs the Gibbs Sampler; such method, or FCS in general, according to van Buuren et al. (2006) is quite robust even when MAR assumption is violated, although their study needs to be replicated, as the authors said. The MCMC uses simulation from a Bayesian prediction distribution for normal data. Allison (2009) describes it as follows : “After generating predicted values based on the linear regressions, random draws are made from the (simulated) error distribution for each regression equation. These random ‘errors’ are added to the predicted values for each individual to produce the imputed values. The addition of this random variation compensates for the downward bias in variance estimates that usually results from deterministic imputation methods.” (p. 82).

The FCS differs from the multivariate normal imputation method (MVN or MVNI) also known as joint modeling (JM) in which all variables in the imputation model jointly follow a multivariate normal distribution. MVN uses a common model for all variables, multivariate normal for continuous var., multinomial/loglinear for categorical var., general location for a mixture of continuous and categorical var., but encounters difficulty when the included variables have different scale types (continuous, binary, …) whereas FCS can accomodate it. Despite MVN being more restrictive than FCS (e.g., the use of binary var. and categorical var. makes the normality assumption even more unlikely), Lee & Carlin (2009) found both methods perform equally well even though their imputation model included binary and categorical variables. Unfortunately, van Buuren (2007) found evidence of bias related with JM approach under MVN when normality does not hold. It is not all clear under which condition MVN is robust.

In the present data, I noticed that the selection of monotonic method instead of MCMC is not effective and SPSS send us an error message like “the missing value pattern in the data is not monotone in the specified variable order”. In this way, we can easily choose which method we really need. See Starkweather (2012) and Howell (2012) for the procedure in SPSS.

When using MCMC, Starkweather and Ludwig-Mayerhofer have suggested to increase the maximum iteration from the default value of 10 to 100, so as to increase the likelihood of attaining convergence (when the MCMC chain reaches stability – meaning the estimates are no longer fluctuating more than some arbitrarily small amount). That means 100 iterations will be run for each imputation. Because the default value is too low, I wouldn’t recommend the “auto” option. But Allison (2002, p. 53) stated however that the marginal return is likely to be too small for most applications to be of concern.

Then, we are given two model types for scale variables, Linear Regression (by default) or Predictive Mean Matching. PMM still uses regression, but the resulting predicted values are adjusted to match the closest (actual, existing) value in the data (i.e. the nearest non-missing value to the predicted value). It helps ensuring that the imputed values are reasonable (within the range of the original data). Given the apparent advantage of PMM (such as, avoiding extreme outliers in imputed values) over the default option, I select PMM with my MCMC imputation method.

The next step is to go to “Impute Missing Data Values” in order to create the imputed data set. All the variables in the model have to be selected. If the missing pattern is arbitrary, we go to Method, Custom, and click on “Fully conditional specification (MCMC)” with max iterations at 100, preferably. Nonetheless, MCMC works well for both monotonic and arbitrary patterns. If we don’t really know for sure about the missing pattern, we can let SPSS decide. It will choose the monotone method for a monotonic pattern and MCMC method otherwise (in this case, the default number of iteration would be too low). Concretely, SPSS (like AMOS) will create a new data set (with new dataset name). The entire procedure is explained in this webpage and this video. See also IBM SPSS Missing Values 20 (pp. 17-23).

When using FCS method, we must also request a dataset for the iteration history. After this, we should plot the mean and standard deviation of the imputed values on the iterations, for each variable separately, splitted by the imputation number. See the manual SPSS missing values 20 (pp. 64-67) for the procedure of FCS convergence charts. The purpose of this plot is to look for patterns in the lines. There should not be any, and they will look suitably “random”.

Last thing, it is extremely important not to forget to change the measurement level of the variables. For example, mom_educ and dad_educ were initially configured as “nominal” while imputation in SPSS only works with “scale” variables, not with “nominal” or “ordinal” measure. We simply have to re-configure these in the SPSS data editor window. Otherwise, SPSS gives such message “The imputation model for [variable] contains more than 100 parameters. No missing values will be imputed.” See here.

In the data editor, at the upper right, we see a list of numbers below “Original Data” going from 1 to 5. They represent the number of imputations (5 being the default number on SPSS) because it’s a multiple (not single) imputation. The data has been imputed 5 times, each time giving us with different imputed values. If we had 50 individuals cases (i.e., 50 rows), clicking on 1 will bring us to the 51th row and the 50 following rows, clicking on 2 will bring us on the 101th row and the 50 following rows, and so on. Finally, the yellow shaded cells show the newly created values.

This new dataset is very special. If we perform an analysis using the new dataset, for example a mean comparison of GPA score with gender group, we will be given a table divided into 7 parts. First, we have the mean value (and other stats requested on SPSS) for the original data, second, the mean for each of the five imputed data, and finally the mean for the pooled of the five imputed data. And the pooled (i.e., aggregated) result is the only one we are interested in when performing analyses on SPSS, unless we want to apply Rubin’s formula. We can also use the SPLIT FILE function with the variable “imputation_” in order to get separate results for each stacked data.

There is another method, called Expectation-Maximization, which overcomes some of the limitations of the mean and regression substitution methods such as the preservation of the relationship between variables and lower underestimation of standard errors, even if it is still present in EM. It proceeds in 2 steps. The E-step finds the distribution for the missing data based on the known values for the observed data and the current estimates of the parameters; and the M-step substitutes the missing data with the expected values. This two-step process iterates (default value=25 in SPSS) until changes in expected values from iteration to iteration become negligible. EM assumes a multivariate normal model of imputation and has a tendency to underestimate standard errors due to the absence of a component of randomness in the procedure. Unfortunately in SPSS, there is no way we can create a clustered data file with EM method. We can only create several separate files.

To perform EM, go to “Missing Value Analysis” and put the ID variable in Case Labels, put the variables of interest in Quantitative or Categorical Variables depending on the nature of the variable (e.g., scale or nominal) and select the “EM” box. There is also an EM blue button which we need to look at, and then we click on “save completed data” and name the new data set. When we click on OK, the output provides us with several tables, notably “EM means”, “EM covariances”, “EM correlations” with the associated p-value from χ² statistics. This is a test of the MAR assumption known as Little’s Missing Completely at Random (MCAR) Test. Because the null hypothesis was that the data are missing completely at random, a p-value less than 0.05 indicates violation of MCAR. As always, the χ² is sensitive to sample size and with large N we are likely to have a low p-value, easily lower than 0.05 due to high power of detecting even a small deviation from the null hypothesis, as I noticed when performing this test which appears completely worthless.

Another method, initially not included in SPSS package, is the Hot Deck. This is the best-known approach to nonparametric imputation (although it does not work well with continuous/quantitative variables) and this means it avoids the assumption of data normality. The hot deck procedure sorts the rows (i.e. respondents) of a data file within a set of variables, called the “deck” (or adjustment cells). The procedure involves replacing missing values of one or more variables for a nonrespondent (donees) with observed values from a respondent (donors) that is similar to the non-respondent with respect to characteristics observed by both cases; for example, both of them have variables x1, x2, x3, x4 with, say, respectively, values of 6, 5, 4, 4, but the donor has x5 with value of 2 while the donee has no value in x5, and so the hot deck will give him a value of 2 as well. In some versions, the donor is selected randomly from a set of potential donors. In some other versions, a single donor is identified and values are imputed from that case, usually the nearest neighbor hot deck. Among the benefits of hot deck, the imputations will not be outside the range of possible values. This method performs less well when the ratio of variables (used for imputation process) to sample size becomes larger, and should probably be avoided in small data because it seems difficult to find donors with good matching in small data, and has also the problem of omitting random variations in the imputation process. Even when multiple imputation is performed, the variance in the pooling process is still underestimated although some other procedures (e.g., Bayesian Bootstrap) can overcome this problem (Andridge & Little, 2010). Myers (2011) gives the “SPSS Hot deck macro” for creating this command for SPSS software. Just copy-paste it as it is. See also figure 3 for illustration of the procedure.

The PMM (semi-parametric) method available in SPSS resembles hot deck in many instances but because it uses regression to fill the data, it assumes distributional normality but has the advantage that it works better for continuous variables. It still adds a random component in the imputation process, preserves data distribution and multivariate relationship between variables. Andridge & Little (2010) argue about the advantages of PMM over hot decks.

Like hot deck, PMM is recommended for monotone missing data, and it works less well with an arbitrary missing pattern, which is probably what we have presently. It is possible that the method I used is not optimal, and in this case I should have selected MCMC with linear regression method, not PMM. Nonetheless, regarding the bivariate correlations of all the variables used, the pooled average does not diverge so much from the original data. Most often, the cells differs very little, with correlations differing by between ±0.000 and ±0.015. In some cases, the difference was ±0.020 or ±0.030. Exceptionally, some extreme cases have been detected, with cells where the difference was about ±0.050. Even my SEM analyses using MI look similar to those obtained with ML (see below). Moreover, linear regression and PMM produce the same results (see XLS). So generally, it seems that PMM does not perform badly in preserving the correlations.

b) Multiple imputation on AMOS.

In AMOS graphics, one needs to select and put the selection of variables we want to impute. Unlike SPSS, AMOS can impute latent variables. All it needs is to construct the measurement model with the observed and latent var.

In Amos (see, User’s Guide, ch. 30, pp. 461-468), three options are proposed : 1) regression imputation, 2) stochastic (i.e., aleatory) regression imputation (also used in SPSS), 3) Bayesian imputation. The first (1) fits the model using ML and then the model parameters are set equal to their maximum likelihood estimates, and linear regression is used to predict the unobserved values for each case as a linear combination of the observed values for that same case. Predicted values are then plugged in for the missing values. The second (2) imputes values for each case by drawing randomly from the conditional distribution of the missing values given the observed values, with the unknown model parameters set equal to their maximum likelihood estimates. Because of the random element in stochastic regression imputation, repeating the imputation process many times will produce a different dataset each time. Thus, in standard regression, the operation looks X^i=b0+b1Zi while in the stochastic we have X^i=b0+b1Zi+ui where ui is the random variation. The addition of the random error avoids the underestimation of standard errors. The third (3) resembles stochastic except that it considers model parameters as stochastic variables and not single estimates of unknown constants.

The first option 1) is a single imputation and should not be used. 2) and 3) propose multiple imputations, could be configured using the box “number of completed dataset” which has a default value of 5. It designates the number of imputed data we want to generate before averaging them. Make sure that the box “single output file” is checked. Because checking “multiple output file” will create 5 different datasets, one for each imputation completed. With single file, the datasets will be stacked together with a variable “imputation_” having 5 values; say, we have data for 50 subjects, thus, rows 1-50 belong to the value 0 in the variable “imputation_”. Then, rows 51-100 belong to 1 in the variable “imputation_”, rows 101-150 belong to 2, and so on. While multiple files create 5 files with each 50 rows, the single file creates 1 file with 250 rows.

Byrne (2010, p. 357) while arguing that mean imputation method is flawed said that the regression imputation also has its limitations. Nonetheless, stochastic regression imputation is still superior than regression imputation. This seems to be the best option available in AMOS. But it is probably not recommended to conduct imputation with AMOS especially when SPSS proposes more (flexible) options.

Now, we can look at the newly created data, which only contains the variables we need for our CFA-SEM analysis. Obviously, it lacks the grouping variables (e.g., “race” in the present case). We can simply copy-paste the variable’s column from the original data set to this newly created data set, or to merge these data sets (->Data, ->Merge Files, ->Add Variables, move the “excluded” variables into the “key variables” box, click on ‘Match cases on key variables in sorted files’ and ‘Both files provide cases’ and OK). When this is done, save it in a computer’s folder before closing the window. There is no need to be concerned by the possibility that the ID numbers (i.e., raws) could have been rearranged in the process of imputation, that is, IDs are no longer ordered in the same way. In fact, SPSS/AMOS keeps the row values in the original order. So, copy pasting does not pose any problem.

2.2.4. Distribution normality and Data cleaning.

a) Checking variables’ normality.

Violation of data normality, whether univariate or multivariate, is a threat even for SEM. This can cause model misfit, although not systematically so (Hayduk et al., 2007, p. 847). And even more. Specifically, skewness affects test of means whereas kurtosis affects test of variances and covariances (Byrne, 2010, p. 103). We can check univariate normality by looking at skewness and kurtosis in SPSS. Both skewness and kurtosis should be divided by their associated standard error, a (positive or negative) value should not be greater than absolute 1.96 in small samples, no greater than absolute 2.58 in large sample (200 or more) but in very large sample this test must be ignored (Field, 2009, pp. 137-139). Indeed, when sample size increases, the standard error decreases. For example, the distribution normality of GPA_overall was perfect in the black sample (N=1132, in the original data set) with respect to the histogram, but skewness and its standard error had values of -0.279 and 0.073, in other words a ratio of -3.82, which clearly departs from an absolute value of 2.58. Nevertheless, a rule of thumb is always arbitrary and, in our case, with samples generally larger than 1000, we don’t use this test.

Now, the concept of multivariate normality is somewhat different. The univariate (outlier) is an extreme score on a single variable whereas multivariate (outlier) is an extreme score on two or more variables. Byrne (2010, p. 103) informs us that univariate is a necessary but not sufficient condition for multivariate normality. In AMOS, we can easily display the “tests for normality and outliers” in the “Analysis Properties” box. Unfortunately, AMOS refuses to perform this test when we have missing values, a condition that applies to all (survey) data sets. In his website, DeCarlo gives SPSS macro for the multivariate test of skew and kurtosis, but I don’t know how that works.

Hopefully, it is still possible to deal with missing data in AMOS by using the “multiple imputation” method. This consists in replacing missing values by substituted, newly created values based on information from the existing data. At the end, we can assess multivariate normality.

We are given the skew and kurtosis univariate values (with their C.R.) for each observed variables. The absolute univariate kurtosis value greater than 7.0 is indicative of early deviation from normality (Byrne, 2010, pp. 103-104), but a value of 10 is problematic and larger than 20 it becomes extreme (Weston & Gore, 2006, p. 735). An absolute univariate skew value should be no greater than 2 (Newsom, 2012) and a value larger than 3 is extreme. With regard to the C.R. (skewness or kurtosis divided by standard error of skewness or kurtosis), it should not be trusted, because of the standard error being too small in large sample sizes. At the very least, we can still compare the C.R. among the variables even if it would be more meaningful to simply look at the univariate kurtosis value. Concerning the multivariate kurtosis critical ratio, C.R., also called Mardia’s normalized coefficient because it is distributed as a z-test, it should not be greater than 5.0. Concerning the multivariate kurtosis, or simply Mardia’s coefficient of multivariate kurtosis, Bollen (1989) proposes that if the kurtosis value is lower than p*(p+2), where p is the number of observed variables, then there is multivariate normality.

AMOS test for normality also gives us the Mahalanobis d-squared values (i.e., the observations farthest from the centroid) for each individual case. The values are listed and start from the highest d² until the lowest d² is reached. A value that is largely distant from the next other value(s) is likely to be a strong outlier at either one of the ends. An illustration that worths 1000 words is given in Byrne (2010, p. 341). As always, the p values associated with the d² values are of no value. With large sample sizes, they will always be 0.000. Gao et al. (2008) mention the possibility of deleting outliers to help achieving multivariate normality but that a large amount of deleted cases would hurt generalizability.

When AMOS lists the number associated with the individual case, this number does not refer to the ID value of the survey data, but the case sorting from lowest ID to highest ID. The column in blue, below :

The mismatch between ID and the case sorting is probably due to the syntax I used for creating the imputed data (filter by race variable). So, for example, the case value (outlier) 1173 suggested by Mahalanobis distance, in my imputed dataset, refers in reality to the number in the blue column, not 7781 under the variable column R0000100 that represents the ID number in NLSY97. Because of this, we need to be careful. Delete outliers by beginning from the highest case value, to the lowest case value. Otherwise, the case ordering would be re-arranged.

For the univariate test, in SPSS, I have used a complete EXPLORE (in ‘descriptive statistics’ option) analysis for all the variables. It shows skewness and kurtosis values with their respective standard error, and as we noted earlier, this test can be ignored. It is probably more meaningful to look at the normal Q-Q plot (violation of normality is evidenced if the dots deviate from the reference fitted line) and detrended normal Q-Q plot (which has the same purpose but just allows us to check the pattern from another angle). Finally, EXPLORE will display boxplots with individual cases that could be outliers. Also displayed as test of normality is the Kolmogorov-Smirnov but this test is flawed and should probably never be used (Erceg-Hurn & Mirosevich, 2008, p. 594).

Regarding ASVAB subtests, normality holds, although AO departs (but not too seriously) from normality. Generally, when the dots depart from the reference fitted line, they do it at the extremities (lower or upper) of the graph. The same applies for Mom_Educ, Dad_Educ and SQRT_parental_income, with no serious violation of normality. Given the boxplots, there was no strong outliers in any of these variables, except Mom_Educ and Dad_Educ (in the black sample only) because there were too much people with 12 years of education and few people with less or more than 12 years, which produced a histogram with an impressive peak at the middle. In any case, this general pattern is quite similar for black, hispanic and white samples. We can conclude there is no obvious deviation from normality given those tests.

Before leaving this topic, always keep in mind that EXPLORE analysis must be performed with option “exclude cases pairwise” or otherwise a large amount of cases in all of the selected variables could be ignored in the process.

b) Choosing SEM methods.

Parameters (i.e., error terms, regression weights or factor loadings, structural (path) coefficients, variance and covariance of independent variables) are estimated with maximum likelihood (ML) method, which attempts to maximize the chance (probability) that obtained values of the dependent variable will be correctly predicted. For a thorough description, go here. ML is chosen because it is known to yield the most accurate results. Other methods include Generalized Least Squares (GLS) and unweighted least square (ULS; requires that all observed variables have the same scale) which minimizes the squared deviations between values of the criterion variable and those predicted by the model. Both ML and GLS assume (multivariate) distribution normality with continuous variables, but other methods like scale-free least squares, and asymptotically distribution-free (ADF), do not assume normality of data. ML estimates are not seriously biased when multivariate normality is not respected (Mueller & Hancock, 2007, pp. 504-505), if sample size is large enough, or “(if the proper covariance or correlation matrix is analyzed, that is, Pearson for continuous variables, polychoric, or polyserial correlation when categorical variable is involved) but their estimated standard errors will likely be underestimated and the model chi-square statistic will be inflated.” (Lei & Wu, 2007, p. 43).